I’ll admit I came to lithium by accident more than 1 year ago. I saw a LinkedIn post, asked who I should talk to, and the answer came back in two words: Antoine Walter.

Antoine runs Don’t Waste Water, has interviewed hundreds of the smartest people in this industry, and spends part of his working days on lithium, leading business development for GF Piping Systems.

I like Antoine's work because he's known for drilling deep into a topic, uncovering layers of context and insights that make the content both valuable and highly relevant.

That's exactly why I started learning about lithium through him.

Before that conversation, I genuinely didn’t understand what lithium had to do with water.

This past week, a very interesting 7th International Congress about Lithium in Latam took place in Argentina.

The key data they shared is literally those:

Lithium demand projected to rise 40x in the next two decades

Global output must grow 5x by 2030 to meet net-zero targets

Energy transition requires over US$116B in lithium investment

Latin America holds +60% of global lithium reserves

Argentina, Bolivia and Chile jointly control ~54 million tonnes

Chile remains the leading lithium producer in Latin America

Chile targets 140k–180k tonnes LCE expansion by 2030

Argentina holds second-largest global reserves (19.3 Mt)

Argentina has 40+ lithium projects in development pipeline

Bolivia aims for 100k+ tonnes/year production by mid-2020s

So I thought it was a great moment to catch-up with the learning journey about Lithium, and why water professionals should pay attention to this field.

You’ll understand once you read below the details.

At the end of the essay you’ll find links to other sources and references to continue your learning journey.

Start with the wall of demand

Everything in this story is driven by one fact: the world needs vastly more lithium than it currently makes, and soon.

The numbers are slippery, lithium gets counted as metal, as carbonate, as hydroxide, as chloride, and people quote whichever suits them, so it’s easy to get lost.

But the order of magnitude is solid. Global production crossed roughly a million tonnes of lithium carbonate equivalent for the first time in 2024, and most forecasts put 2030 demand somewhere between 2.5 and 3 million tonnes.

In round terms, the industry has to roughly double or triple its output inside a decade, with some scenarios pushing the multiplier higher if electric-vehicle incentives hold.

That is the engine behind every other thing in this essay.

Electric cars, grid-scale storage, the batteries inside everything…they all want lithium, and the supply curve has to bend hard to meet them.

Where lithium actually comes from

Here’s the first thing that surprised me: there are really two lithium questions, and people may confuse them.

The first is mining—getting lithium out of the ground. Roughly 40% comes from hard rock in Australia.

A big slice comes from the “lithium triangle”—Chile, Argentina, and Bolivia—though if we’re honest it’s mostly Chile, some Argentina, and a Bolivia that has barely started producing. The rest comes from China. Add it up and about 95% of world production sits in those few places.

The second question is refining—turning that raw material into the battery-grade stuff.

And here is the punchline: more than 90% of refining happens in China. The lithium hydroxide and lithium carbonate that actually go into batteries are, overwhelmingly, made in China.

Once you separate those two questions, the geopolitics writes itself.

The whole game

Antoine put it in a way I keep repeating to people.

China doesn’t really want to sell lithium. China would rather sell batteries. And medium-term, China doesn’t even want to sell batteries—it wants to sell cars.

Follow that logic and the vulnerability is obvious.

If China decides its national interest is best served by keeping its lithium and its battery cells and exporting finished vehicles instead, then a carmaker in Europe or North America that didn’t secure its own supply is left with no lithium, no batteries, and therefore nothing to sell.

An entire automotive industry can be hollowed out not by losing a price war on cars, but by losing access to a metal three steps upstream.

This is why “where does my lithium come from” has stopped being a procurement question and become a strategic one.

It’s also why countries are scrambling to build domestic supply chains—and why those efforts collide with local realities.

Bolivia, sitting on enormous reserves, has leaned toward China: there was a tender that everyone could enter, and somehow only Chinese companies were selected.

Chile runs much of its resource through a national mining company holding a 51% stake.

Argentina is province by province—some welcome lithium, some forbid it outright.

Same triangle, three completely different rulebooks.

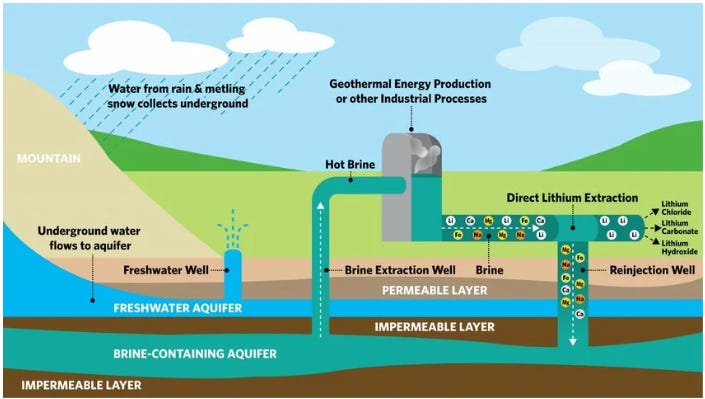

Four ways to get it out of the ground

Now to the part that finally connected lithium to our world.

Hard rock. You mine a rock called spodumene (first time I heard of…), which is only about 0.8–1% lithium, and concentrate it (using, among other things, dissolved-air flotation) into something around 6% before it goes to refining. Australia, China, Canada, and a famously contested deposit in Serbia have spodumene.

Brines. In the lithium triangle, you pump up brine and pour it into vast evaporation ponds—essentially the same technique as harvesting table salt. The sun does the work, and what’s left behind is lithium chloride, again around 6%. Cheap on capex, but slow, and it raises real problems I’ll come back to.

Clay. Newer, and what the US is pursuing around Nevada and Texas. The processing route looks a lot like the spodumene route, just with clay as the input.

Direct Lithium Extraction (DLE). This is one interesting. DLE uses water-treatment technology—membranes, ion exchange, adsorption and desorption—to pull lithium out of brines too dilute for the old methods. We’re talking 200–400 parts per million, sometimes as low as 60.

When waste becomes the resource

The DLE example that stuck with me is oil fields. When you pump up a litre of oil, you bring up something like eight litres of water with it.

For a century that water was pure waste—a disposal cost. It turns out some of it carries 40–60 ppm of lithium. If you can extract that, the waste becomes a by-product becomes a revenue stream.

That is the exact same arc we keep talking about in water: the thing you used to pay to throw away turns out to be valuable if you have the technology to unlock it.

Technologies that were always too expensive for water—overkill if all you’re doing is making drinking water—suddenly become competitive when the prize is one specific, high-value element of the periodic table.

And it’s not a one-shot opportunity. It seems baattery-grade lithium has to be 99.99% pure.

Getting from 6% to five-nines is a long road of chemical and water treatments on the brine side, or roasting-and-leaching followed by more chemistry and water treatment on the rock side.

Every step is a place where membranes, ion exchangers, and adsorption come into play. For a water-technology company, exciting opportunities.

Why it takes a decade and a billion dollars

If demand is screaming and the prize is huge, why isn’t supply catching up faster? Because mines are slow and brutally capital-hungry.

A hard-rock mine takes roughly 5–10 years to open.

An evaporation-pond operation takes 10–15.

DLE at full commercial scale is so new that nobody honestly knows yet—the projects are ramping, not proven.

And every exploration drill can cost around a million dollars just to find out whether what’s underground is even worth chasing.

So how do you fund a decade of pure cost? Two routes.

Some companies go public absurdly early, raising money on the stock market while still in exploration.

Others sign offtake agreements: a carmaker buys the future lithium before a single tonne exists. General Motors did exactly this with Lithium Americas’ Thacker Pass project in Nevada—committing well over a billion dollars across stages for a 38% stake and access to production, even as the project is still being built. (In a sign of how strategic this has become, the US government itself took a roughly 10% position in the company in late 2025.) Stellantis has chased European lithium the same way. The one big holdout is Tesla, which believes its market position makes it immune to a shortage.

The driver underneath all of it: gigafactories. There are dozens planned across Europe and North America, and the rough rule is one gigafactory needs about one lithium refinery to feed it. Build the factories and you’ve made an enormous, standing bet that the lithium will show up.

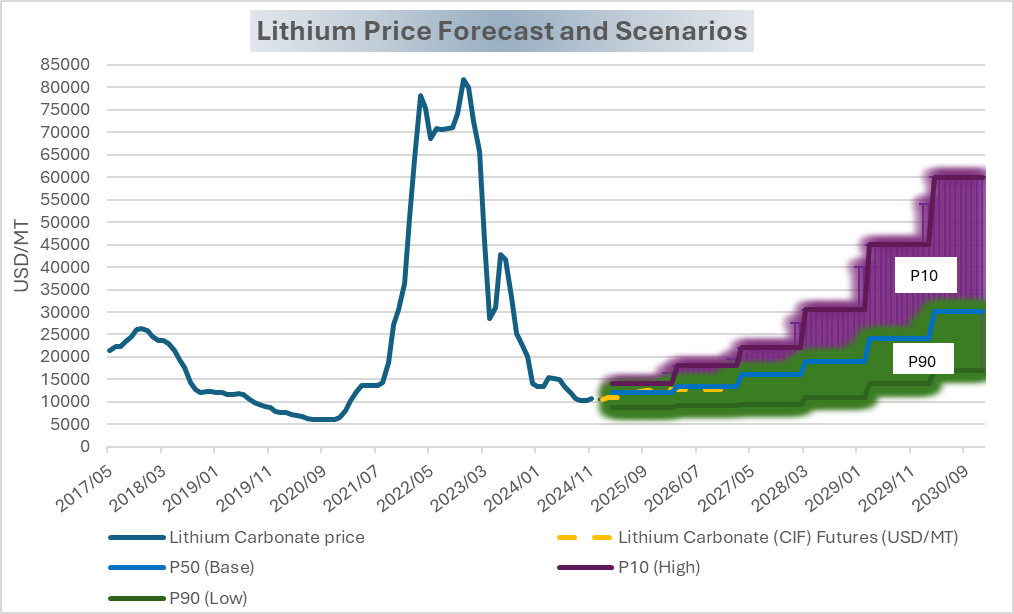

Hovering over the economics is a price that has been on a rollercoaster.

Pre-COVID, a tonne of lithium ran around $4,000–5,000. A year after COVID it spiked toward $80,000–100,000.

It has since crashed back to roughly the $10,000–15,000 range—still well above where it began, but a long way down from the bubble, and enough to push marginal projects into delay or bankruptcy.

Several Canadian projects, advanced but undercapitalised, simply died during COVID, which is part of why the rebound in demand hit such a thin supply base.

The Bolivia problem, and the skull on the wall

Two things complicate the romantic picture of “just evaporate brine in the sun.”

First, chemistry. Bolivia has enormous lithium but a lithium-to-magnesium ratio roughly 30 times worse than Chile’s.

When you try to precipitate the magnesium out, you drag lithium out with it, so process efficiency collapses—from the 40–45% you might see in Chile or Argentina down to something far lower.

Abundant sun and resource can offset that, but it’s a real handicap.

Second, water. Brine isn’t drinking water, but it is water, and the salars sit in some of the most arid places on Earth.

Draw too much from the bottom of the system and the whole water table can fall. Antoine described seeing, in Argentina, walls painted with the word “Litio” beside a skull—and, across the road, communities cheering the same lithium for the jobs it brings to places that never had any.

Two faces of one coin. That tension, more than any spreadsheet, may decide where the industry can actually operate.

Where this is heading

Lithium was and probably is one of the most exciting frontiers in water, precisely because almost nobody in water is calling it a water story yet.

The demand wall is real.

The geopolitical squeeze is real.

And the technical answer—how you economically extract a few hundred ppm of a metal from brine, or recover it from oil-field wastewater, or polish it to XXX purity—may be, fundamentally, a water-treatment problem.

I went in knowing nothing. I came out convinced this is a corridor of opportunity that water professionals are walking past without recognising the door.

Why a busy engineer makes a podcast

I couldn’t end without the part of the conversation that wasn’t about lithium at all, because it’s the part that explains why people like Antoine exist to teach the rest of us.

He started Don’t Waste Water during COVID, almost by necessity. He’d just moved into a business-development role for water and wastewater, right as lockdown made it impossible to meet anyone.

So he turned the constraint into the method: reach out to the people he knew, put the conversations in public, and let that visibility pull in the people he didn’t yet know.

(It wasn’t even his first podcast—an earlier one walked through 55 sales books after he was thrown, untrained, into selling a treatment plant for Suez and survived on Sales for Dummies and sheer nerve.)

What I loved most was his honesty about why he keeps going.

The catchphrase is that listening to the show gives you a “water MBA” but, he told me, the water MBA he’s really earning is his own.

An hour a week with a superior mind, 250 weeks in a row, knowledge poured straight into his head.

He called it egoistic, self-centred, and meant it as a compliment to the format.

The fact that thousands of other people benefit too is, in his telling, a happy side effect.

That landed, because it’s exactly how I think about this work. People ask whether I’m wasting or spending time and money on it.

I use a different word: investing. Even in the scenario where the subscriber count stays at zero, the return—in learning, in conversations like this one, in the simple joy of staying curious—is already positive.

You do it because you like it, or you don’t do it at all.

Which, now that I think about it, is the same logic as the oil-field brine. The thing everyone else treats as a cost turns out, with the right perspective, to be the most valuable thing in the room.

Thanks everyone for reading, sharing and engaging.

Here a few links to continue this topic:

Interesting video from Antoine: