I want to open another edition of the Reuse series, our cheapest molecule.

This time deliberately step off the technical ground. Not membranes and treatment trains, but commercial and market intelligence.

What does the market expose about reuse that the process flow diagram never will?

As usual, I go back to one of my favourite sources.

Partly because some of these people I almost consider good friends, they’re genuinely great peers, and I just like listening to them.

Some time ago I had dinner with Keith Hays, one of the co-founders of Bluefield Research, here on this side of the Atlantic, and the kind of work they do has always fascinated me.

At the end of this publication, you’ll find links to these contacts. They regularly share extremely interesting perspectives and genuine value on LinkedIn. I wish I had more time to consume all the great content the share out there, and I’m sure I’ve missed many, but I highly recommend connecting with and following them.

The Future of Water podcast is also one of my regular check-ins every couple of weeks, usually while I’m at the gym (pretending I do exercise). It consistently offers valuable insights and thought-provoking conversations. Highly recommended.

So in this conversation with María Cardenal, from Bluefield’s Barcelona office, to talk reuse.

The invisible craft behind the data

Most of us in this sector spend our days heads-down inside our own scope.

I know I do, a purchase order lifecycle here, a commissioning sequence there, one brine outfall…

We start to believe the work just arrives on our desk. It doesn’t.

Behind every clean number in a report there’s an enormous amount of invisible labour: understanding the market, sizing it, separating the big players from the small ones, working out who is operating where and why.

María’s company does exactly that — market intelligence. Market sizing, valuations, business research, the short two-page notes when a deal or a project breaks, and the deeper reports.

It runs on a subscription model with a database layer (the Data Navigator, which Keith first told me about) that clients filter and query.

The geographic core is the US, Canada and Europe; the verticals run from municipal water to industrial — pharma, beverage, meat, metallurgy, mining, and increasingly water for data centres and energy — plus a whole digital-water practice.

What I found most honest was when I asked María about the hardest part of her day-to-day.

Her answer wasn’t glamorous: it’s finding the information.

There’s a lot of it out there, but it’s scattered, hard to digest, hard to interpret, and sometimes it simply isn’t there at all.

She described disappearing down a rabbit hole — Alice in Wonderland, in her words — pulling thread after thread, then doing the sanity check with peers to make sure the conclusion holds.

Actually, it is quite a similar operating system to creating The Water MBA.

That’s the unglamorous truth of intelligence work, and it’s exactly why I respect it. The value isn’t the data. It’s the judgement that turns scattered noise into something you can actually decide with.

Reuse is a market, not a technology

Here’s the conceptual shift that runs underneath everything: the wastewater plant is no longer a treatment endpoint.

It’s becoming a provider — a source of water, of energy, of recovered resources.

Once you see it that way, reuse stops being an engineering question and becomes a market question.

María laid out a clean four-part framework for why reuse actually happens in a given place:

Drivers — environmental: water scarcity, the need to conserve water (potable or agricultural), and protecting coastal aquifers from seawater intrusion.

Regulatory requirements — the macro frame. The EU Water Reuse Regulation (2020/741) has applied directly across all member states since June 2023, setting harmonised minimum quality standards for reclaimed water in agricultural irrigation. On top of it, the recast Urban Wastewater Treatment Directive (2024/3019), adopted at the end of 2024.

Local requirements — infrastructure, technical capacity, and geography. Reusing water halfway up a mountain (pumping uphill, burning energy) is a different proposition from a coastal industrial cluster where the user is next door.

End use determines treatment — and this is the commercial crux. Agriculture, street cleaning, industrial cooling and potable reuse each need a different treatment level. There is no single right answer.

Notice what’s missing from that list: “build the best plant.” The commercial lens reframes the whole problem.

It isn’t can we treat the water? — we can, the technology exists. It’s match the treatment to the use, build the pipe, and figure out who pays.

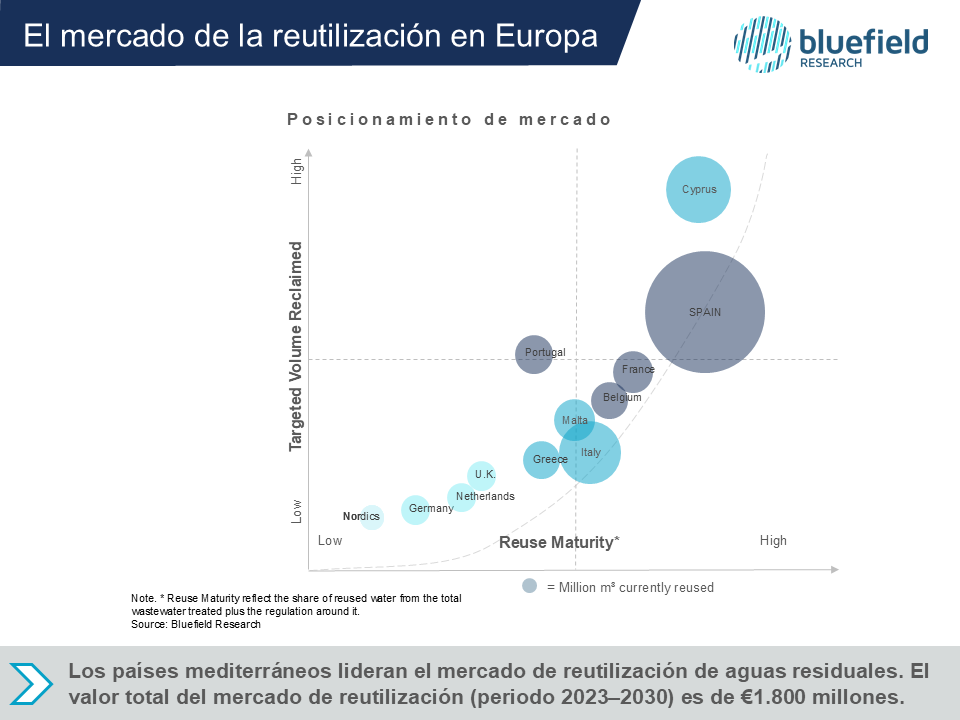

The numbers: leadership is relative, headroom is enormous

Back in 2023 Bluefield went so deep on European reuse that one report had to become two, covering 11 countries.

Their estimate for the total European water-reuse market over 2023–2030 was around €1.8 billion.

The headline most people expect is that Spain leads Europe, and it is correct. The country reusing the most water on the continent.

But here’s the figure that should keep us humble: that leadership amounts to reusing only about 14% of our wastewater.

The European “leader” is leaving most of the resource on the table.

Within Spain it’s wildly uneven — Murcia reuses something like 98%, almost all of it for agriculture, a number you simply don’t see anywhere else.

So “leader” is a relative word, and the more useful way to read those numbers is as headroom.

Layer in Bluefield’s map of incremental water scarcity — the regions sliding into stress on current climate trends — and the addressable market isn’t just deep, it’s geographically expanding.

Places like Málaga, already squeezed between population, tourism and climate volatility, are tomorrow’s mandatory adopters.

Belgium: where intelligence beats intuition

If you want to see why market intelligence earns its fee, look at Belgium.

Intuition says reuse is a Mediterranean story, sun, drought, fires.

Belgium has none of that branding, no specific reuse regulation on the books, and rain almost every day. And yet it sits in the top tier of the European reuse ranking.

Why? Because the country is under genuine water stress despite the rain, heavy urbanisation and industrialisation mean the soil simply can’t retain what falls, and the aquifers are limited.

And crucially, the demand is being pulled by industry, not policy: reuse around the Port of Antwerp, automotive plants near Brussels running closed loops for cooling and cleaning, potato-processing lines that drink enormous volumes of water.

One car factory near Brussels co-financed the reuse project that connected the local treatment plant to its site.

The lesson is one of the most commercially important in the whole topic: regulation is one driver, not the driver. Industrial demand and plain economics can lead reuse forward in a place no policy map would have flagged.

If your intelligence only tracks regulation, you’d miss Belgium entirely.

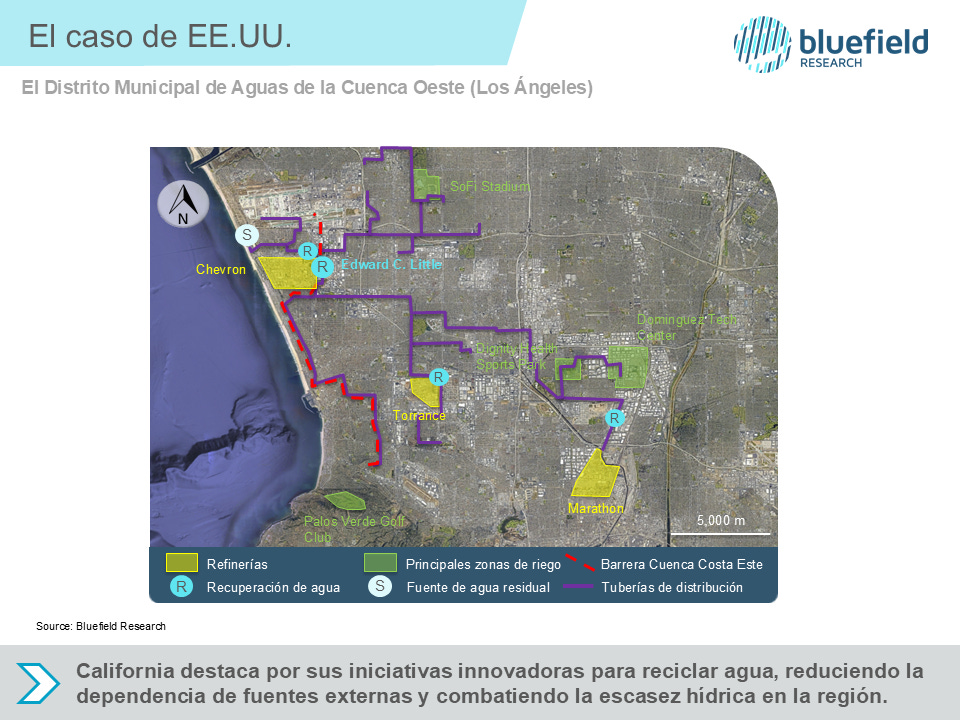

Los Angeles: the masterclass

LA has been at this since the 1980s. Not a ten-year sprint; a forty-year programme.

Bluefield frames US reuse as a five-rung maturity ladder: no reuse and drawing on natural sources; non-potable reuse; indirect potable reuse (IPR); studying direct potable reuse; and finally approved direct potable reuse.

LA runs the full stack and does three things at once:

Industrial supply — reclaimed water piped to refineries and industry instead of potable water.

Irrigation — parks, golf courses, stadiums, urban green space.

A seawater intrusion barrier — injecting reclaimed water into coastal aquifers to physically hold back the saltwater that creeps in as those aquifers are drawn down. It’s the same risk Barcelona lives with, solved with reused water.

And it runs through purple pipes — the colour code (used globally mostly too) that tells any worker on site instantly that the line carries reclaimed water.

I love that detail, because it captures the part of this business everyone underrates: it’s mostly invisible.

The plants aren’t in the city centre, the pipes are underground, and then someone tells you the water you flushed is coming back to irrigate the food you’ll eat.

Of course the public hesitates. That’s why IPR and DPR are 20-to-30-year programmes built on pilot after pilot, redundancy after redundancy, and patient confidence campaigns.

The technology is the easy part. Trust is the slow part.

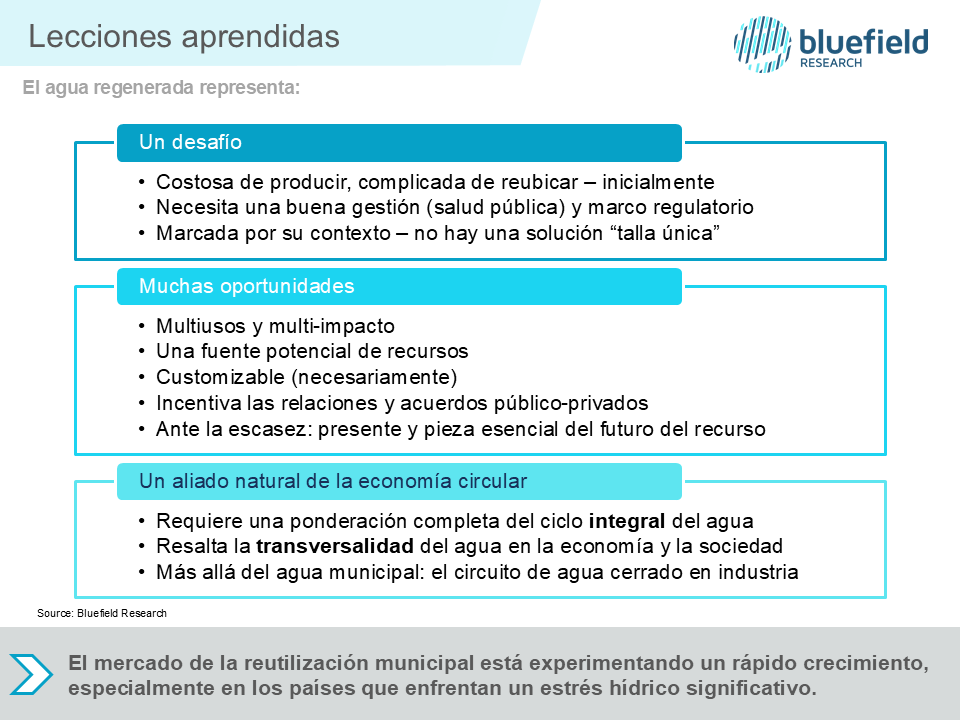

The four commercial truths

Here’s what the market actually exposes as per Maria point of view:

Infrastructure is the cost, not the technology. We obsess over treatment, but the pipe that redirects the water to a user who can actually take it is often the bigger line item. That Belgian factory paid for the connection, not the treatment.

There is no one-size-fits-all — and over-treating is a mistake. Pushing every drop to potable grade is inefficient if it’s only cleaning streets.

Higher treatment means more capex, more opex, more energy. Matching grade to use is the business model.

Who pays is the hardest equation in the room. Public and private benefits are tangled together.

The intangible upside is real — freeing potable water for human use, enabling local industry, ESG and corporate water targets, lower emissions from industrial closed loops — but it’s genuinely hard to put on a single business plan.

PPPs, incentives and reuse tariffs exist precisely because no one party captures all the value (you’ll read a great piece about this on next Tuesday)

Time is the price of entry. These are inter-generational assets. Anyone hoping to walk in, hit one technical key and flip the market is in the wrong business. We’re building for the next generation — which, by the way, is also why the demand is almost guaranteed for us :)

See you soon

The commercial reading is simple to state and hard to execute: scarcity sets the floor, regulation sets the frame, but industrial demand, infrastructure financing and public trust decide who actually builds.

That’s the part the membrane datasheet will never tell you, and the part people like María and the Bluefield team spend their days, heads-down in the rabbit hole, working out.

My thanks to María Cardenal for sharing it so generously, and to Keith and the wider Bluefield team.

The real privilege of our community is the peers and friends who’ll sit across a dinner table and tell you what the data actually says.

If you’re heading to Marrakech, come find me. Let’s talk reuse!

Continue on your own through the next sources:

Maria Cardenal, Antonio del Olmo, Keith Hays, the Bluefield website, and The Future of Water Podcast.